Key Points:

-

In the second quarter of 2023, the average monthly payment for a new car purchase hit $733.

-

Over 17% of consumers financed a vehicle with a monthly payment of $1,000 or more in the second quarter of 2023.

-

Locking in a lower auto loan payment might involve shopping around for a better rate, choosing a cheaper car, or sticking it out with your current vehicle.

The average monthly car payment on a new car hit $729 in the second quarter of 2023. That’s a significant bite out of any household budget.

Let’s explore the trend of rising auto payment costs and strategies you can pursue to lock in lower auto ownership costs.

Rising Car Payment Costs

Between the first quarter of 2019 and the second quarter of 2023, the average interest rate on a 60-month new car loan rose from 5.27% to 7.81%.

A vehicle is a critical way to get to work for a large number of Americans. Since driving is a common way for Americans to get around and the average cost of a vehicle is thousands of dollars, it might not be surprising that the majority of new vehicle purchases are made possible through financing.

On average, drivers signing up for new car financing in the second quarter of 2023 financed $40,356 for an average term of 68.5 months. The average monthly payment stands at $733. For used cars, the average monthly cost was $569 for an average amount of $29,665 financed.

Why Are Car Payments Rising?

Transportation costs take up a significant portion of American household budgets. While transportation has always been a big expense, the rising cost of auto loan payments has pushed this portion of average household budgets higher.

Below is a closer look at some of the reasons why auto loan payment amounts are on the rise:

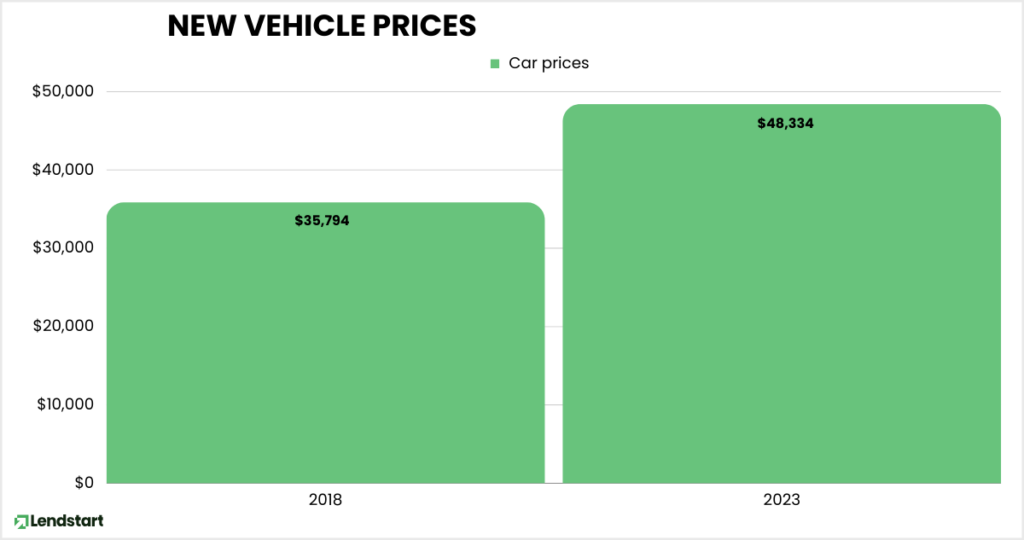

- Higher car prices: The average price of a new car was $48,334 in July 2023. That’s significantly higher than the average new vehicle price of $35,794 in 2018. As the cost of a new car rises, average monthly payments continue to rise.

- Higher interest rates: Between the first quarter of 2019 and the second quarter of 2023, the average interest rate on a 60-month new car loan rose from 5.27% to 7.81%.

A combination of rising car prices and higher interest rates has led to the perfect storm of higher monthly payments for auto loan shoppers.

Auto Loans Related Articles

Highest-Paying Jobs in 2024 That Don’t Require a College Education

Effect of Tariffs on Businesses and Consumers: A Look at the Pros and Cons

Understanding the 2025 Tax Bracket and Standard Deductions

How Much Silver Should You Own?

How to Avoid Higher Auto Loan Payments

Average car payments are on the rise. But the good news is that you can take action to lower your auto loan payment costs. Explore the strategies below:

- Save for a bigger down payment: A big down payment will lower the total amount you need to finance, which can lead to a more affordable monthly payment. Consider building your savings in a high-yield savings account to maximize your savings.

- Consider a used car: The average monthly cost of a used car is significantly cheaper than a new car. Consider moving forward with a used car to lower your transportation costs.

- Stick it out with your current car: If you have an older vehicle, it might not be time to upgrade yet. If you can, consider driving your current vehicle and use the opportunity to save up for a larger down payment on your next vehicle.

- Shop for the best rate: As you explore your auto loan options, don’t forget to shop around for rates. Locking in a lower rate can help you save thousands over the course of your loan. Explore the lowest rates available today.

The Bottom Line

For many American households, getting by without a vehicle isn’t an option. But paying an average of over $700 per month for a vehicle isn’t possible for many households either. If you are in the market for a vehicle, explore all of your cost-saving options.

Before diving into a car purchase, make sure to find the best interest rate and loan terms by shopping around.

Article Topics

Sarah Sharkey is a personal finance writer with a Master's in Management from the Hough School of Business at the University of Florida. She enjoys helping people make better financial decisions and has written for numerous personal finance publications, including Money Under 30, Business Insider, and The College Investor. Sarah enjoys traveling, hiking, and reading when she is not writing.