With COVID-19 cases rising and as supply chain and labor challenges continue to be an issue for the housing market, Americans may see mortgage rates trend upwards, experts are predicting. While, for now, there isn’t much change to mortgage rates, there are several factors that may come into play when asking the question, “Will mortgage rates rise?” — the publishing of the U.S. Department of Labor September employment report and the debt ceiling facing Congress.

Currently, APR rates sit between a little over 2% and 3%; however, Americans may soon — perhaps starting in November — have to say goodbye to those low rates as inflation starts to take its toll.

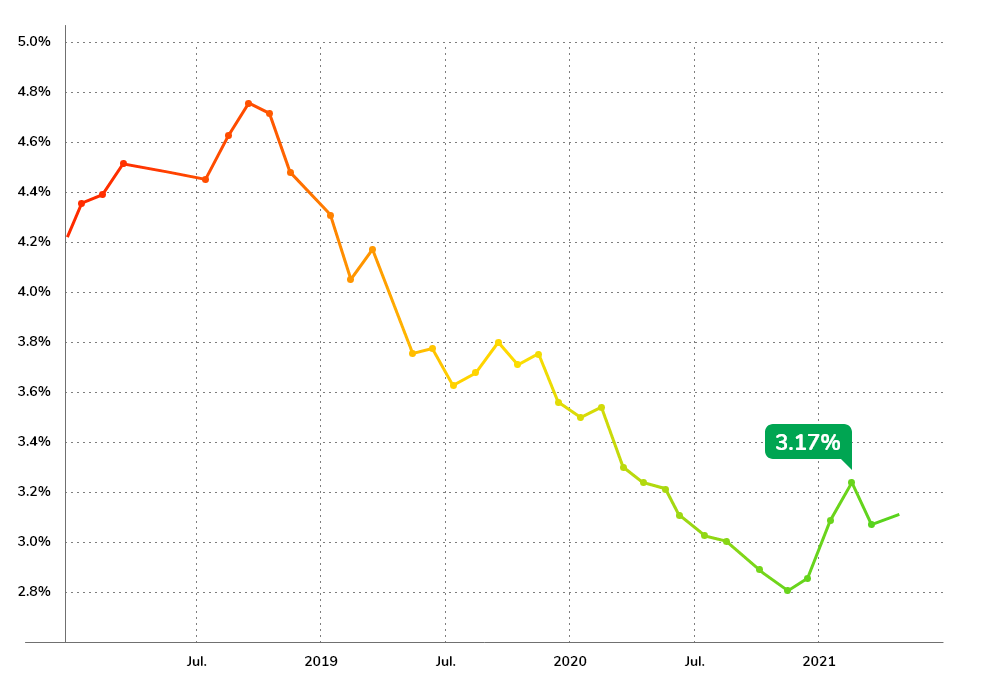

Mortgage Rates Forecast for November 2021

On November 3, the Federal Reserve may make a decision on how to proceed with its purchases of mortgage-backed securities (MBS). The Federal Reserve does not typically set mortgage rates. However, it’s been an influential force in keeping those rates low recently by spending $40 billion each month on MBSs.

As COVID-19 cases continue to serve as a challenge to economic recovery, inflation is starting to increase with it and “largely reflecting transitory factors”, according to a statement from the Federal Reserve's September 22, 2021 meeting. However, the Federal Reserve also noted that vaccinations and economic policies have led to more economic activity and employment.

“If progress continues broadly as expected, the Committee judges that a moderation in the pace of asset purchases may soon be warranted,” the Federal Reserve announced at the meeting.

For now, since the Federal Reserve is continuing these efforts in purchasing MBSs, Americans probably won’t see much fluctuation in mortgage rates. However, if the economy continues to show growth, the Federal Reserve may back off buying MBSs, experts are saying. Some economic experts suspect that the Federal Reserve may even announce a plan to taper off at its next meeting, November 3. As a result, borrowers may ultimately see mortgage rates slowly climb starting in November.

Mortgage Rate Predictions for the rest of 2021

According to Freddie Mac’s quarterly forecast, Americans may see 2021 close out with 30-year-fixed mortgage rates around 3.4%. This prediction on rising mortgage rates is reliant on multiple factors. These events may cause Americans to see changes to mortgage rates throughout the remainder of 2021:

- Mortgage rates may be impacted by the Department of Labor’s September employment situation report, set to be released October 8. The August 2021 employment situation was, in the words of a Fannie Mae report, “disappointing.” While the unemployment rate dropped to 5.2%, small businesses reported difficulty in filling positions. While the August findings could have been a “blip,” if the September employment report shows a similar trend, the “tight labor market” may continue to spell out economic challenges. However, if the employment situation is positive, it could encourage the Federal Reserve to taper off its purchases of MBSs, experts believe.

Another factor that could impact the mortgage rates prediction for the remainder of 2021 is the outcome of the ongoing $28.4 trillion debt ceiling debate in Congress. If federal lawmakers don’t come to an agreement in the next several weeks, Congress could hit its debt ceiling as soon as October 15, according to a report by the Bipartisan Policy Center. If the U.S. federal government were to default, this could mean that the country’s credit ratings and demand for Treasury bonds could fall, ultimately leading to increased mortgage rates, researchers predict.

Mortgage Rate Forecast for 2022

If the Federal Reserve tapers off its purchases of MBSs to keep mortgage rates low, Americans may see more of an impact in 2022 rather than 2021. This is because the committee may not announce its decision until its November 3 meeting. While this change in the wind may be felt starting in late 2021, more of the brunt might be felt in 2022 as the housing market adjusts, according to experts. In the words of a Freddie Mac report, “while we forecast rates to increase gradually later in the year (2021), we don't expect to see a rapid increase.”

However, the Federal Reserve isn’t the only factor that can impact mortgage rates going into 2022. In fact, it may even clash with other challenges the housing industry is facing.

The COVID-19 pandemic continues to be disruptive to home construction. Housing market issues with the supply chain and labor shortages — which limit the number of homes available to be sold compared to the demand — aren’t expected to end anytime soon, some experts believe. In fact, they’ll likely extend into 2022, according to some researchers.

“We also expect inflation to remain elevated through much of next year,” Doug Duncan, Fannie Mae senior vice president, and chief economist, said in a Fannie Mae report. “Affordability remains a challenge, even with mortgage rates near historic lows; if the pace of income growth doesn’t keep up with inflation and interest rates rise more than expected, we’d expect housing activity to slow from our current projections.”

After a volatile year for the housing market in 2020, the industry experienced a seesaw of low home sales to an “unsustainable rebound,” according to a report by the National Association of Home Builders (NAHB). New home sales have since cooled.

“Home prices are up 20% from a year ago due to higher construction costs, and these price hikes are a risk for housing affordability as we approach the end of the year,” said Robert Dietz, NAHB chief economist, in the report.

However, despite these challenges, Freddie Mac’s latest quarterly forecast report shows optimism in the housing market, though its mortgage refinance rates forecast predicts that refinancing homes will slow as a result of higher mortgage rates going into 2022.

While in the report, Freddie Mac does acknowledge that housing prices are the “highest they have been in 131 years of data dating back to 1890,” it does predict that pricing will start to moderate. Freddie Mac expects to go from full-year house price growth of 12.1% in 2021 to 5.3% in 2022.

“High house price growth has been supported by increased demand due to low mortgage rates, disposable after-tax income that has risen during the current recession and a major shortage of housing supply relative to our population,” the Freddie Mac forecast stated. “The increase in house price growth will be less transitory than the increase in consumer prices, as the U.S. housing market will continue to struggle with a shortage of available housing for many months to come.”

Common Mortgage Rate Strategies

The writing is on the wall, experts are saying: mortgage rates will most likely go back up sooner rather than later, so the window for snagging those low mortgage rates may be narrowing for borrowers looking to purchase a home soon. While it makes sense to pursue these rates while they’re still this low, borrowers should avoid jumping the gun and hopping on a loan until the time is right for them to make a purchase.

In the meantime, there are strategies Americans can utilize that may help them capitalize on low rates.

- Explore mortgage rate marketplaces: Try to avoid settling for the first low rates you see advertised. Often, those rates are geared toward borrowers with excellent credit scores and the finances to put down large down payments, so some borrowers may not qualify for rates as low as advertised. Secure the best offer for your credit and financial situation by comparing the best mortgage rates on an online marketplace like Lendstart. This can make comparing rates, fees, and terms much more convenient so it's easier to lock down the best deal.

- Consider refinancing: Freddie Mac’s mortgage refinance rates prediction forecasts that refi rates are going to get less attractive to borrowers once mortgage rates start to increase again. If borrowers have been pondering refinancing their homes for a while now, it may be wise to take advantage of low rates before they start increasing toward the end of 2021 and into next year. By doing this, you could potentially save money in the long run, especially if you purchased your home before the COVID-19 pandemic at a higher rate.

- Look into buying a second home: In March 2021, Federal Housing Finance Agency (FHFA) limited Fannie Mae and Freddie Mac’s capacity to offer loans for second homes. In mid-September, however, the FHFA and the U.S. Department of the Treasury suspended that measure which may make it easier for borrowers to purchase a second home or investment property at a lower rate than usual. Though, there’s no telling how long this policy suspension will last.

With political and economic events influencing the US economy, higher mortgage rates may be on the horizon for new homeowners for the remainder of 2021 and into 2022. Since there’s a chance the housing market won’t see these rates again for a while, some borrowers may be tempted to sign up for a new home loan prematurely. Borrowers should weigh their options and consider their timing carefully as that may make a difference in how much money they end up spending on their mortgage overall.

Disclaimer

The content is provided “as is”. The content is not, nor shall it be taken as professional or financial services or advice. We are not a financial institute, insurance broker or agent. Your use and reliance on any of the information provided therein should be done solely at your own risk. We highly recommend contacting and consulting a financial advisor prior to taking any financial decision. We will not be responsible for any damages which may occur as a result of your use of the content available therein. We make no warranty that any information available is true, reliable, or accurate.

Article Topics

Jayson Derrick has been writing about all topics related to investment and personal finance since 2013. Prior to that, he was in charge of a news desk for a prop trading firm.