CIT Bank advertises that accounts can be opened in 3 simple steps:

- Provide information: You’ll need to provide your address, phone number, email, and social security number.

- Fund account: Saving and checking account products require a $100 minimum deposit. You can transfer funds by electronic transfer, mail-in check, or wire.

- Confirmation: Receive confirmation via email and enjoy the CIT online banking benefits.

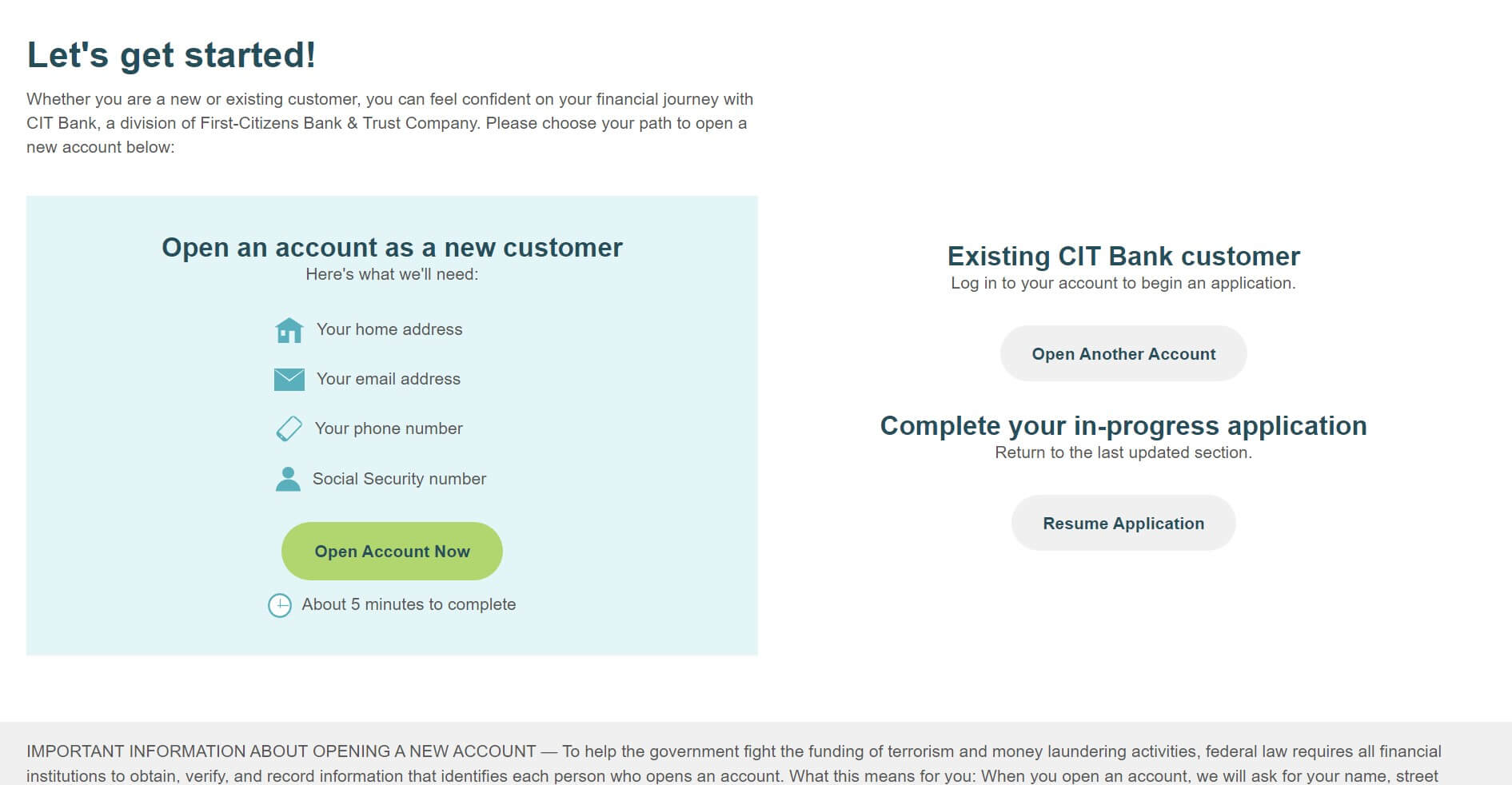

The first step is to navigate to the CIT Bank website and find the green button in the upper right corner that says “Open Account.” Click that, and you will be taken to a page where you can start a new application as a new customer, start a new one as an existing customer, or resume an incomplete one.

Next, choose the type of account you’d like to open. You can open an account for yourself or a custodial account for a minor. You also choose from the different savings, checking, money market, or CD accounts you’re interested in opening.

After choosing your account type, you’ll be taken to a page asking for personal information, such as your name, date of birth, email address, social security number, and your mother’s maiden name.

Then, they will ask for a phone number and your physical address.

You could save and exit at this point, and you’ll get an email with a link that allows you to come back and finish the process at any time, although it does say that incomplete applications are deleted after 30 days – so don’t delay too long. The next page asks for citizenship and employment information.

After clicking to continue, you’ll be presented with a page that shows all the information you’ve entered thus far. You’ll be asked to review that information and confirm that it is correct. If it is correct, click the “Save and Continue” button. If changes need to be made, there are Edit links you can click to modify any of the previously entered information.

Next, you’ll be asked if you want to add a joint user to your account. Then, you’ll be taken to the application’s account set-up section.

The following page is where you agree to the bank’s terms and conditions, privacy policy, and schedule of fees. Two tick boxes, and you continue to the IRS withholding screen, where the bank asks if you are subject to backup withholding by the IRS. After moving on from that page, you are asked to confirm your taxpayer identification number (TIN), which will be a social security number for most. You will then be directed to a page where you can create your online login credentials.