Form 941, the Employer's Quarterly Federal Tax Return, is one form you might come across as a business owner. It is a crucial form that communicates to the Internal Revenue Service (IRS) about the payroll taxes you've collected from your employees. Knowing how to fill it out accurately and on time can save you from potential headaches. By following this guide, you can help ensure that you are filling out Form 941 correctly, accurately, and on time.

What is Form 941?

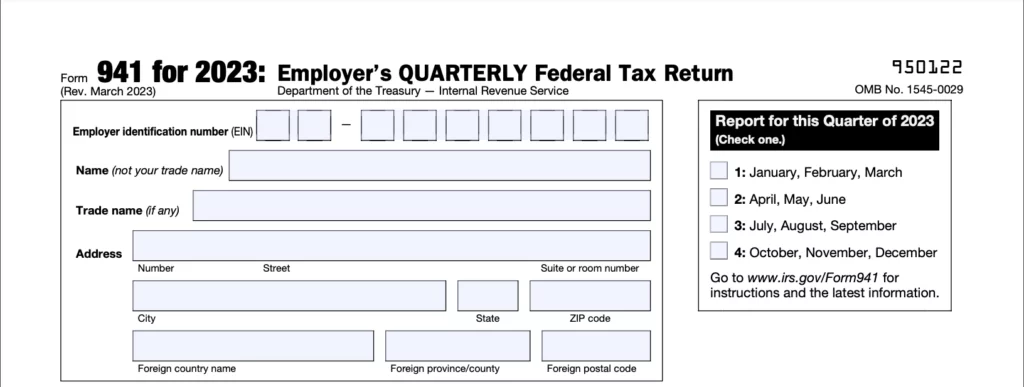

Form 941 is a quarterly tax form that employers must file with the IRS to report the wages they paid to their employees and the taxes they withheld from those wages. The form also reports the employer's share of Social Security and Medicare taxes. Form 941 is due on the last day of the month following the end of each quarter, and it covers the wages paid and taxes withheld during the quarter.

If you're an employer who pays wages to employees and those wages are subject to income tax withholding or Social Security and Medicare taxes, then Form 941 is for you.

Step-by-Step Guide for Completing Form 941

Navigating the maze of tax forms can be daunting, especially when the form in question is as crucial as Form 941. It is here where we will break it down for you. With patience and organization, you can accomplish this task more quickly than you might think. Let's take it step by step to simplify the process and more manageable for you.

Step 1: Gather Relevant Documents and Information

Before diving into Form 941, you'll need some information at your fingertips. You'll want to have details about your business and employees ready, including:

Your Business ID

- The number of employees

- The total wages you've paid out

- The total amount of Social Security and Medicare taxes paid

By having all this information at hand, filling out the form will be much smoother. Remember, preparation is key when dealing with tax forms.

Step 2: Provide Employer Information

Next, you'll need to supply specific information about your business. This is where your Employer Identification Number (EIN) comes in. You'll find a dedicated space on the form for this - it's essential to fill it out correctly.

Having your EIN handy ensures that your tax report is correctly linked to your business. It’s like a social security number, but for your business.

Step 3: Calculate Tax Liability for the Reporting Quarter

Now we move on to the more intricate parts of Form 941. You'll need to compute your tax liability for the reporting quarter. Don't worry, you have already collected the necessary information in step one.

This calculation involves a few components:

- Determine the total wages subject to Social Security and Medicare taxes

- Calculate the total tax withheld from the employee's wages

- Factor in any adjustments, if necessary

There are dedicated sections on Form 941 to report these numbers within Part 1.

Step 4: Tally Up Deposits and Payments

After calculating the tax liability, you'll need to take stock of the deposits and payments your business made during the quarter. Form 941 has specific lines where you'll report these figures in part 2:

Remember, these entries should reflect the total tax deposits made during the specific quarter, including Federal income tax withheld from employees and both the employer and employee share of Social Security and Medicare taxes.

Step 5: Declare Adjustments and Credits

The final step in completing Form 941 involves declaring any adjustments and credits. You can write this information into Part 3 of Form 941.

Understanding what adjustments and credits apply to your business situation is crucial. Consider engaging the help of a tax professional. Their expertise could help ensure accuracy, and they might help spot adjustments or credits you could otherwise miss. Notably, any mistakes could lead to overpaying or underpaying your taxes.

Submitting the Form 941

With all the previous steps complete, you're now ready to submit Form 941. The IRS accepts submissions either electronically or by mail. The method you choose is up to you, but remember to ensure that it's submitted before the deadline for the quarter.

In addition, if you are considering using a third-party designee or not, ensure you complete part 4 of form 941:

As well as do not forget to sign and complete part 5:

Completing Form 941 might seem daunting, but it can be manageable when broken down into these steps. It starts with gathering the necessary documents and information and providing your employer information. The heart of the form is calculating your tax liability for the quarter, tallying your deposits and payments, and declaring any applicable adjustments and credits.

Remember, these tasks require accuracy and attention to detail. Mistakes could lead to penalties, so taking the time to get it right is essential. And if in doubt, you may find it helpful to work with a tax professional to guide you through the process.

When is Form 941 Due? Important Filing Deadlines

Completing Form 941 is one part of the process, but ensuring it arrives at the IRS on time is equally important. The deadlines are quarterly, given the nature of the form. Specifically, for each quarter of the year, the Form 941 is generally due by the last day of the month following the end of the quarter.

To clarify, the deadline for the first quarter (January to March) is April 30th. The second quarter (April to June) is July 31st. The third quarter (July to September) has a deadline of October 31st, and the fourth quarter (October to December) is due by January 31st of the following year.

Penalties may apply if Form 941 is filed late or contains errors, so strive to avoid those situations. The IRS can charge interest on the amount of tax not paid by the due date, and this interest rate changes every quarter.

Navigating tax forms, including Form 941, can be complex and sometimes overwhelming. If you're uncertain or overwhelmed, consider seeking assistance from a tax professional. They can help you ensure your Form 941 is accurate, complete, and submitted on time, potentially saving you from costly penalties and stress.

Driving Toward Success: The 9 Essentials for Car Loan Refinance Approval

Why every pet owner needs pet insurance

Highest-Paying Jobs in 2024 That Don’t Require a College Education

Effect of Tariffs on Businesses and Consumers: A Look at the Pros and Cons

Form 941 vs. Form 941-X: What’s the Difference?

Form 941 and Form 941-X serve distinct but related purposes for businesses. While Form 941 is the vehicle for reporting your payroll taxes and employee wages each quarter, Form 941-X is its amendment counterpart. Essentially, if you discover errors or necessary adjustments to a previously filed Form 941, Form 941-X is the tool you'll use to correct them.

You might find yourself needing to file Form 941-X in a variety of scenarios. For instance, if you realize that you overlooked claiming certain tax credits, such as the Employee Retention Credit, or if you discover an error in the reported total wages or tax calculations, Form 941-X is your route to setting things straight with the IRS.

- Aspires to provide the fastest refund possible

- Live tax experts available to help

Conclusion

Completing Form 941 is crucial to managing a business's financial responsibilities. By understanding its purpose, who it's for, and the key steps involved in completing it, you're better equipped to navigate this important task. Remember, due diligence in gathering information, accurately completing all parts, and adhering to submission deadlines can contribute to smoother tax reporting. If in doubt, don't hesitate to seek assistance from tax professionals to help ensure your Form 941 is accurate and timely. Moreover, being aware of the differences between Form 941 and Form 941-X and when to use each can prevent potential headaches down the line. This guide aims to make the complex world of business tax filing a bit more approachable. Remember, staying informed and organized can make tax reporting less daunting and more manageable.

Article Topics

Matthew is a freelance financial copywriter with 14+ years in financial services. He holds a Bachelor of Science degree in Economics with business and finance options and is a CFA Charterholder. He is from Vancouver, Canada, but writes from all over the world.